By Adam Pagnucco.

With MCPS unions pressing for full funding of the school system’s requested budget and the county council resisting the full ten percent property tax increase recommended by the county executive, the budget is headed to a showdown largely driven by how much money will be appropriated to the schools. MCPS claims that without at least eight of the nine increments placed by the council on the reconciliation list (equivalent to $178 million), it will be unable to fund its union contracts. In a budget discussion on Friday, several participants wondered how much money MCPS had “under the couch cushions.”

What’s the answer?

The true answer is known only to MCPS management. But we can get a glimpse of it by reading the school system’s comprehensive annual financial reports (CAFRs). These are wonderful documents containing much information not disclosed in MCPS budgets, including balance sheets and account statements. While they are published with a lag time (roughly six months after the end of each fiscal year), they are as close as the public will ever come to seeing just how much money MCPS has.

Let’s zero in on fund balance, which the Governmental Accounting Standards Board (GASB) defines as “the difference between assets and liabilities in a governmental fund.” There are different kinds of fund balances, with some more easy to spend than others. GASB offers guidance to governmental entities in classifying and reporting these balances. MCPS’s most recent reporting of its fund balances occurred in its FY22 CAFR, which applies to the fiscal year ending on June 30, 2022.

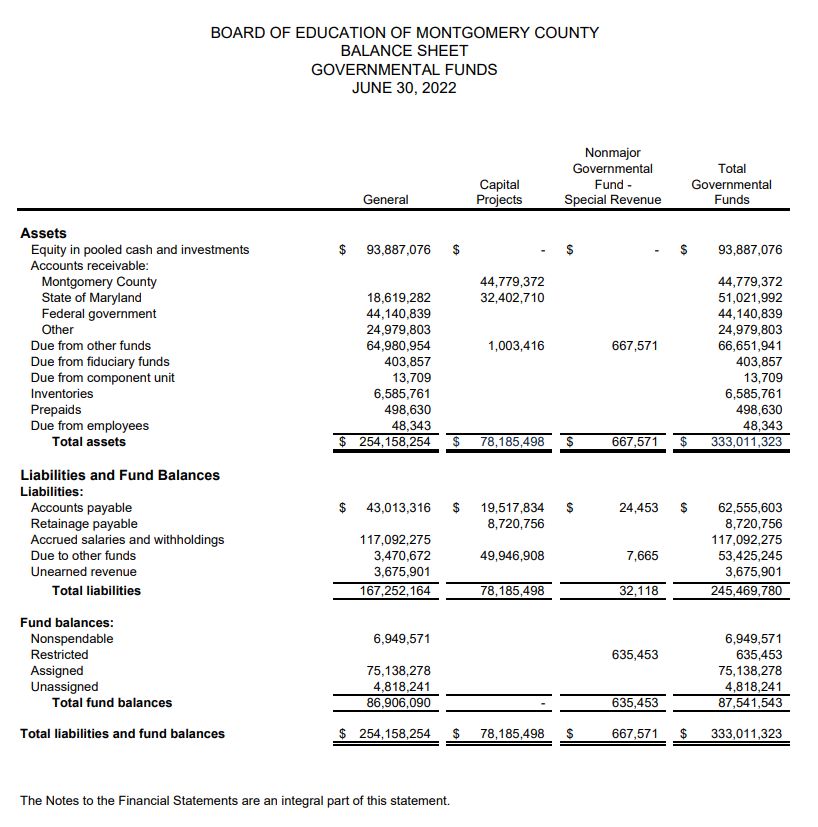

The screenshot below shows MCPS’s balance sheet on 6/30/22 and can be found on page 36 of its FY22 CAFR. Note the tabulations of fund balance at the bottom.

At first glance, MCPS showed a total fund balance of $87.5 million. That’s a lot of money and is roughly equivalent to four of the eight $22 million increments that MCPS says it needs to fund its collective bargaining agreements. But there is a huge caveat – MCPS can’t actually tap all of this money. We need to understand the different categories of fund balance to know how MCPS can – or can’t – use it.

Nonspendable Fund Balance: $6.9 Million

MCPS defines nonspendable fund balance as “Amounts that cannot be spent because they are either (a) not in spendable form or, (b) legally or contractually required to be maintained intact, such as a permanent fund. Not in spendable form includes items that are not expected to be converted to cash, such as inventories and prepaid items.”

Scratch this money, folks. MCPS can’t be expected to sell off its inventories to support its operating expenses. It can’t be used.

Restricted Fund Balance: $635,453 (in a special revenue fund)

MCPS defines restricted fund balance as “Amounts for which constraints have been placed on the use of the resource either (a) externally imposed by creditors (such as through a debt covenant), grantors, contributors, or laws or regulations of other governments, or, (b) imposed by law through constitutional provisions or enabling legislation. Special Revenue Fund resources are restricted to use for the Instructional TV program only. The restriction exists by law under a Cable Franchise Agreement established by Montgomery County Code, Chapter 8A, Cable Commission Law.”

Scratch this money, too. MCPS can only use it for its cable TV programming due to the county’s cable franchise agreement. It can’t be diverted to other uses.

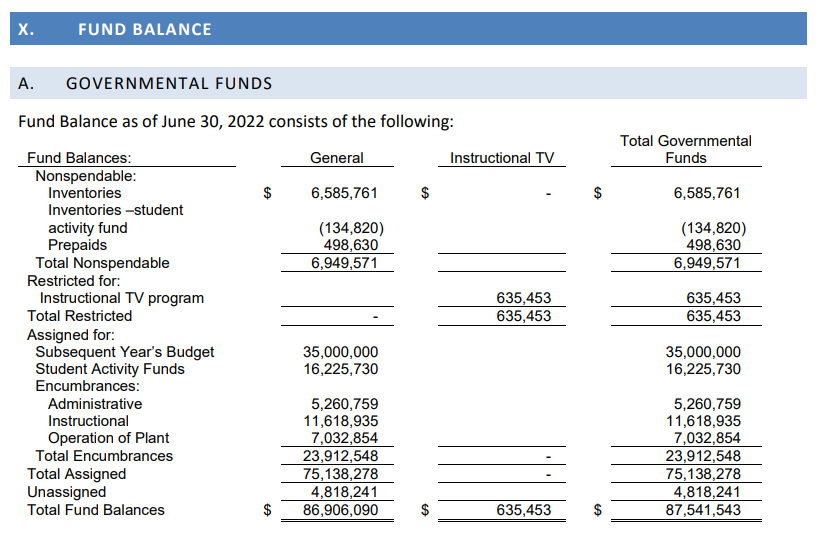

Assigned Fund Balance: $75.1 Million

MCPS defines assigned fund balance as “Amounts that are constrained by the government’s intent to be used for specific purposes, but are neither restricted nor committed. The intent should be expressed by: (a) the governing body itself, or, (b) a body (for example, a budget or finance committee) or official to which the governing body has delegated the authority to assign amounts to be used for specific purposes. This category includes resources the Board have expressly assigned to specific purposes. An assignment may be determined and amended, by the superintendent of schools, or their designee.”

This money has been allocated to specific purposes by the school board. It can also be reallocated to other purposes by the school board or the superintendent. The table below from page 67 of the CAFR shows more detail of this particular fund balance.

Of the $75 million, the school board assigned $35 million to next year’s budget, $16 million for student activity funds, $5 million for administration, $12 million for instructional purposes and $7 million for operation of plant. If the $16 million for student activity funds came from collections of student fees, it would be unfair to transfer that to other purposes. The rest of the money could be moved at the discretion of the board.

Unassigned Fund Balance: $4.8 Million

MCPS defines unassigned fund balance as “This classification is the residual amount of the general fund balance which represents all spendable amounts that have not been restricted, committed, or assigned to specific purposes. In other funds, the unassigned classification can only be used to report a deficit balance resulting from overspending for a specific purpose for which amounts had been restricted, committed, or assigned.”

While not a lot of money, this is essentially everything else.

It’s worth noting my prior findings – that MCPS never spends its full budget for instructional salaries, that it regularly transfers instructional salary money to other purposes and that its fund balance has soared in recent years. Check out the screenshot below from page 117 of the FY22 CAFR that shows MCPS’s ten-year fund balance history.

Given all of these facts, it’s apparent that MCPS has significant financial flexibility. It’s also reasonable to ask why the school system needs big increases while it sits on big fund balances and does not spend all the money it already gets for instructional salaries. Perhaps now that the council president has asked for transparency and the school board has replied that it is already transparent, all of the above can be discussed in public.